SharpSpring: With Great Upside Comes Great Risk

SharpSpring: With Great Upside Comes Great Risk

Uncle Ben was a value investor

5-Bullet Summary:

SharpSpring is a cloud-based marketing automation platform focused on digital marketing agencies.

SharpSpring’s strategy is to leverage agencies as distribution partners to sell an increasing number of licenses to small-to-medium businesses (SMBs), boosting average recurring revenue.

SharpSpring has grown revenues at ~25% CAGR over the last three years, reaching $22.7mm in sales in 2019. However, the company faces increasing customer acquisition costs, decreasing gross margins, and high churn rates.

The business is attractive in many ways (growing industry, clear potential for margin expansion, low capital requirements, and capable management team), but SharpSpring still has to prove its business model.

In a fragmented industry with low barriers to entry, business risk is high. I prefer to lean on the safe side, waiting for a better entry point and an attractive risk-reward ratio.

SharpSpring is trading at $7.34/share vs. my fair value estimate of $6.25/share.

One of those spidermen will buy SharpSpring after reading this report

SharpSpring (SHSP): With Great Upside Comes Great Risk

SharpSpring is a cloud-based digital marketing automation platform. The company provides software-as-a-service (SaaS) to digital marketing agencies and small-to-medium businesses (SMB). SharpSpring focuses on digital marketing agencies as distribution partners: the company sells licenses to agencies, which can then resell to their clients.

Founded in 2012 by Rick Carlson (current CEO) and Travis Whitton (current CTO), SharpSpring launched its software in 2014. In August of that same year, SharpSpring was acquired by SMTP, an e-mail relay delivery service. In 2015, SMTP changed its name to SharpSpring and Rick Carlson became CEO. Soon after that, the company divested its other assets to focus on the SharpSpring product.

SharpSpring’s client base includes 2,000 agencies and 500 direct customers. The platform is used by 9,000 businesses. In November 2019, SharpSpring acquired Perfect Audience from Marin Software (NASDAQ: MRIN). Perfect Audience is a digital and social media advertising platform with more than 1,600 customers. With this acquisition, SharpSpring hopes to complement its marketing technology stack and exploit cross-selling opportunities.

What’s Marketing Automation?

Marketing automation software provides tools to attract and engage leads (marketing jargon for potential customers). Common marketing automation features include automated e-mails and workflows, landing pages and forms, A/B testing, and social media tracking.

Underlying the value of marketing automation software is the concept of inbound marketing. Here’s HubSpot’s CEO explaining the difference between inbound and outbound marketing:

“Outbound marketing is when a marketer reaches out to people to see if they're interested in a product. For example, this could include door-to-door sales or cold calling where a sales rep or marketer approaches someone without knowing if he or she is even a qualified lead. Inbound marketing is a strategy where you create content or social media tactics that spread brand awareness so people learn about you, might go to your website for information, and then purchase or show interest in your product.” Brian Halligan

Industry Overview

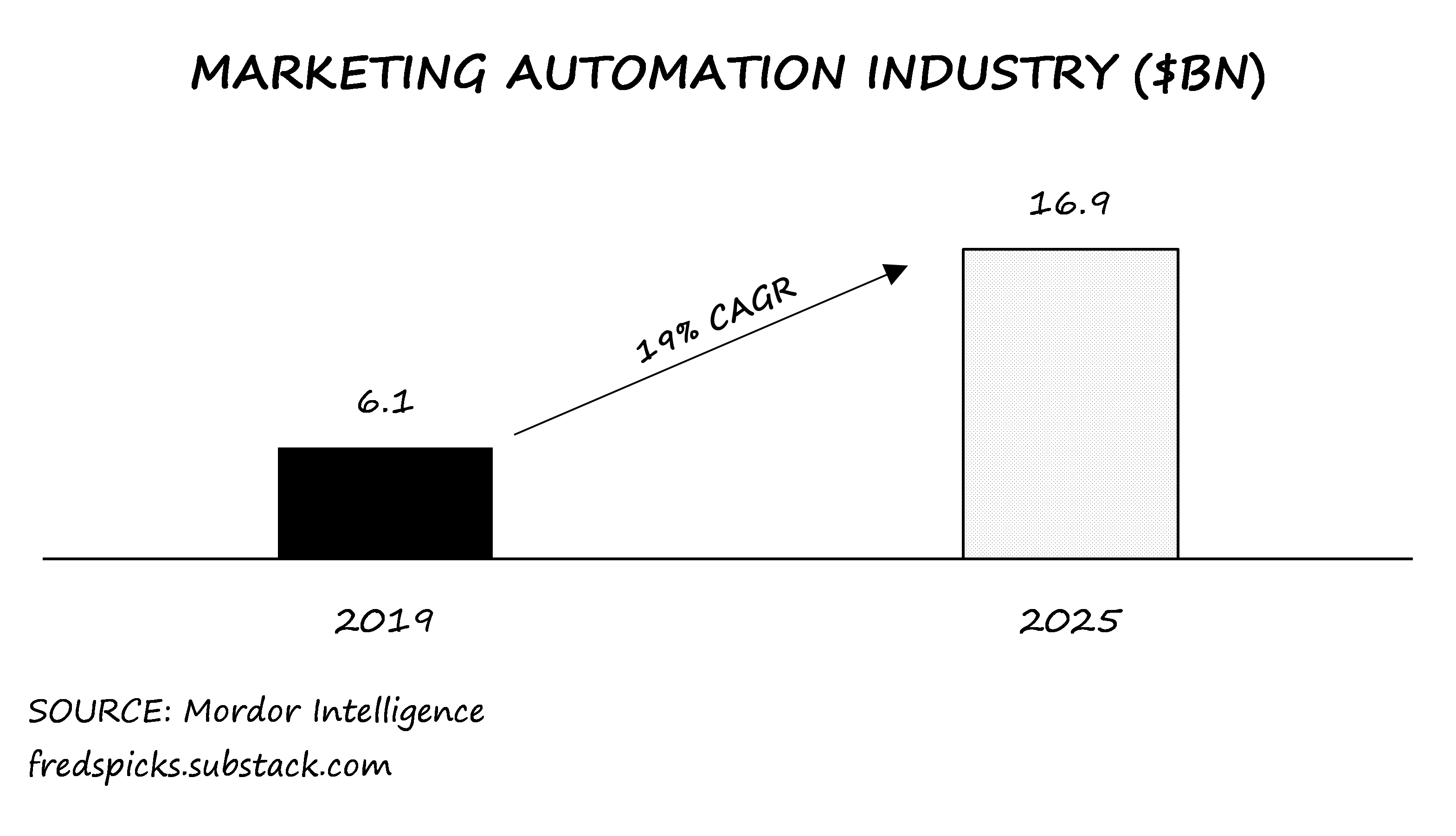

The global marketing automation industry is expected to grow at a 19% compound annual growth rate (CAGR) from 2020 to 2025. Digital ad spending is increasing as companies gain access to more data on consumer behavior and the means to target those consumers individually. Marketing automation software helps companies spend those dollars efficiently.

The industry is competitive and fragmented. There are hundreds of players providing marketing automation software, and there are thousands of players providing other marketing technology applications (e.g. e-mail marketing, video marketing, SEO, CRM, sales automation, etc.).

Source: chiefmartec.com

Industry fragmentation points to low barriers to entry, but there’s a nuance here. Companies focused on enterprise marketing automation, such as Marketo (Adobe) and Eloqua (Oracle), offer comprehensive software and an integrated suite of applications better suited for large organizations. It’s harder to compete at the enterprise level because these are large, one-stop-shop providers, and customers are stickier.

For SMBs, the value of integrated applications from a single provider is lower. SMBs have unique needs and need cheaper solutions, so they use applications from different providers and integrate them. Easy integration with other apps is a valuable feature of marketing automation software.

Marketing automation for SMBs invites competition. SMBs aren’t sticky customers because they are flexible and can easily change between applications. As such, it’s easier for an entrant to develop a solution and grab a share of the market. Barriers to entry are much lower in the SMB segment than in the enterprise segment.

SharpSpring is in the SMB segment. Some of SharpSpring’s main competitors are HubSpot, Act-On (private), Pardot (SalesForce), ActiveCampaign (private), and InfusionSoft (private).

SharpSpring competes with these companies through low prices, a comparable product, and a strategy that focuses on digital marketing agencies. Though competitors also offer some kind of partnership program for agencies, none of them target agencies as their main strategy.

Advantages of Agency Strategy

Digital marketing agencies function as distributors of SharpSpring’s platform. If successful, this strategy leads to:

Constant Revenue Increase

Agencies can continually expand, increasing SharpSpring’s revenues as they sell more licenses to different clients.

Lower Customer Acquisition Costs (CAC)

SharpSpring can focus its sales and marketing spending on agencies instead of diluting its efforts on the overall SMB segment.

Lower churn rates

It’s harder for agencies to change platforms once they are used to SharpSpring and are collecting monthly fees from their clients.

Value Proposition to Agencies

SharpSpring offers lower-priced month-to-month subscriptions (as opposed to annual contracts). According to the company, its software costs 3x to 5x less than its main competitors in the SMB segment (HubSpot, Act-On, and Pardot).

Comparing prices in this industry is a hustle. Companies offer different packages with different functionalities at different prices, and there are different volume usage fees (number of contacts, users, or e-mails sent), onboarding fees, and support fees. Complex pricing hinders clients’ ability to figure out which platform offers the best solution according to their needs.

Despite this price opacity, a comparison of SharpSpring’s average revenue per user (ARPU) against HubSpot indicates SharpSpring's lower-price claim is right.

In addition to lower prices, SharpSpring lets agencies resell subscriptions at whatever price they want and provides a fully customizable platform (agencies can put their color pattern and logo). These are attractive features as agencies can pay lower prices, own the relationship with their clients, look more professional, and make a buck in the process.

Are Lower Prices Good for SharpSpring?

On the one hand, lower prices should attract more customers. They should, but there’s no guarantee: prices aren’t transparent, so much of that benefit gets lost.

For example, SharpSpring recently announced a program to pay for HubSpot Partner Program fees (HubSpot charges $3,600 for agencies wanting to join its partner program). SharpSpring is doing that partly because it wants to signal its cheaper price.

A more attractive benefit from lower prices is untapped pricing power. From an investing perspective, untapped pricing power is awesome. Warren Buffett agrees.

“The single most important decision in evaluating a business is pricing power. If you've got the power to raise prices without losing business to a competitor, you've got a very good business. And if you have to have a prayer session before raising the price by 10 percent, then you've got a terrible business.” Warren Buffett

SharpSpring’s pricing power is being tested in 2020. The company increased prices by +30% at the beginning of the year for agencies that have been using SharpSpring for more than a year. A successful price increase (that is, no material change in churn rates) will reduce risks and add weight to SharpSpring’s investment case.

What About the Quality of SharpSpring’s Software?

SharpSpring is among the top-rated platforms in the industry (see here and here).

SharpSpring has a good product, but it’s not as comprehensive or well-known as HubSpot’s. That’s expected because HubSpot has been around since 2005. SharpSpring came almost a decade later. HubSpot is further along in its product development pathway.

Marketing automation software companies are always adding features to their platforms. SharpSpring is no exception. For example, the company recently implemented chatbots, sales dialers, and video calls.

Having said that, different businesses have different needs. SharpSpring is a low-priced competitor and has a differentiated strategy (focus on agencies). In a short period, SharpSpring reached the #2 position in the industry as measured by agency customers, indicating its product and strategy are competitive in that vertical. Note that there are +50k digital marketing agencies in the US, leaving plenty of room for growth.

SharpSpring’s Key Drivers

There are two: Customer Acquisition Costs (CAC) and Lifetime Value of Customers (LTV). CAC is how much a company spends to acquire a customer. LTV is the total value it extracts from a customer.

LTV must be higher than CAC. Otherwise, what’s the point of attracting customers? The higher the LTV/CAC ratio, the better.

According to SharpSpring, its LTV/CAC ratio is 6.8x. Let’s check that calculation.

CUSTOMER ACQUISITION COSTS (CAC)

SharpSpring calculates CAC as all-in sales and marketing costs (S&M) from a given period divided by the number of customers added in the subsequent period.

SharpSpring assumes CAC of $7.4k. That’s optimistic because the company’s average CAC from 2017 to 2019 is actually $8.3k. That’s because its CAC spiked to more than $10k in 2019.

Two possible explanations for that spike:

1) According to SharpSpring, the company faced inefficiencies in its sales process (number of demos being scheduled). Management says it has addressed this issue and that CAC should go back to historical levels.

2) SharpSpring is facing increased competition and having to pay more to acquire customers (vis-a-vis paying HubSpot Partner Program fees to attract agencies).

I don’t know the right answer. Maybe both of them are right. In my valuation, I assume SharpSpring’s CAC will gradually converge to $8.5k. Given the company’s historical CAC, I think it can partially reduce S&M costs even amid competitive pressures.

LIFETIME VALUE OF CUSTOMERS (LTV)

SharpSpring considers the LTV as the average lifetime gross profit contribution discounted to present value. The company doesn’t consider operating expenses in that calculation. As such, LTV relies on ARPU, gross margins, and churn rate assumptions.

Churn rates

SharpSpring Assumption: A 40% churn rate after two years of customer relationship and a 60% churn rate after 3 to 4 years. Further out, the company assumes immaterial churn rates.

My Take: SharpSpring’s annual churn rates from 2017 to 2019 varied from 35% to 45%. First-year churn rates are higher than that because older cohorts have lower churn rates. As such, SharpSpring’s churn rate assumption is too optimistic: 40% over 2 years vs. the historic rate of +40% over 1 year.

As cohorts get older, SharpSpring’s churn rates should trend lower. The longer a client stays with SharpSpring, the lower the probability it will leave it. Here’s what I consider in my valuation:

ARPU

SharpSpring Assumption: Starts with $600/month, grows to $900/month in 18-24 months and to $1,400/month in 36-48 months. These assumptions don’t consider the ~30% price increase the company implemented in January 2020.

My Take: It makes sense to consider ARPU growing overtime for an initial cohort of clients. If agencies are staying longer with SharpSpring, it means they are using the platform and probably selling it to more clients. For each license sold in excess of the first three licenses included in a standard package, agencies add $200/month in ARPU. SharpSpring considers that agencies add ~4.5 licenses to their base in 18-24 months and ~7 licenses in 36-48 months.

That passes my sniff test and it’s supported by historical numbers: SharpSpring’s average monthly price per agency has increased from $555 in 2016 to $740 in 2019.

Out of caution, my assumptions are more conservative than SharpSpring’s. I don’t consider SharpSpring’s recent price increase because I don’t know how it will affect churn rates. I’ll follow up on that metric throughout 2020.

Here’s what I’m considering now:

Gross Margins

SharpSpring Assumption: SharpSpring doesn’t disclose this metric, but management has commented that it’s gross margin target is +80%.

My Take: SharpSpring’s gross margins hover around 70%. Gross margins peaked in Q4/18 at 72.5% and declined in 2019, as SharpSpring hired account managers to improve service to agencies and try reducing churn rates. Some costs included in SharpSpring’s Cost of Sales, like support and hosting infrastructure, benefit from operating leverage. Therefore, gross margins should increase with customers.

As a comparison point, HubSpot has gross margins of +80% and a long-term target of 81-83%. However, HubSpot’s 2014-2015 margins were similar to SharpSpring’s. As such, SharpSpring has a credible path for margin expansion if it keeps growing its customer base and taps its potential pricing power (which is already trying to do).

I assume SharpSpring’s long-term gross margins are 75%.

MY LTV/CAC CALCULATION

My LTV is close to half of the higher range of SharpSpring’s assumption ($50k). The LTV calculation is highly sensitive to the inputs I mentioned. An LTV of $50k is possible, but I think it’s too optimistic.

I calculate an LTV/CAC of 3.15x, less than half of SharpSpring’s assumption of 6.8x.

Interpreting Churns Rates and ARPU

SharpSpring’s churn rates look incredibly high compared to other SaaS industries. That’s a fair point of concern when evaluating the company.

High churn rates can be partly explained by SharpSpring’s target market. The company targets small digital marketing agencies, which in turn sell to SMBs. Smaller businesses are unstable. HubSpot faced similar problems. Over time, as SharpSpring’s customer base grows older, its churn rates should decrease.

High churn rates can also be partly explained by faulty customer service. For example, according to SharpSpring, a key indicator of whether an agency will stay as a customer is if the agency sells the platform to an anchor client during the early months of the relationship with SharpSpring. That’s why SharpSpring has recently made an investment in account managers, individuals that, among other things, work with agencies to help them drive those sales early.

Again, I note that competition in the SMB segment is fierce and customers are less sticky. SharpSpring must act differently and execute well if it aims to decrease churn rates.

There’s another point to make about churn rates. They reflect logo attrition, that is, losing a certain percentage of clients. That doesn’t directly translate into revenue loss, as staying customers may increase ARPU overtime. The net effect of how much revenue is lost (kept) is called net revenue attrition (retention).

According to SharpSpring’s model, net revenue retention is ~100% after a cohort completes two years with the company (SharpSpring’s avg. agency partner’s age is currently ~19 months). The company expects net revenue retention of ~100% because it assumes that, as agencies grow older, ARPU increases, and churn rates decrease.

SharpSpring just recently started reporting the net revenue attrition metric, which is high: 5.70% in Q4/19 and 3.60% in Q3/19. That means that, for a full year, SharpSpring’s net revenue retention should be 80 to 90%. Similar to churn rates, that metric is concerning. As a point of comparison, HubSpot had a revenue retention rate of 82.9% in 2013, and it reached ~100% in 2017.

In my valuation, I assume SharpSpring will approach an avg. annual net revenue retention of 90%-95%.

Management

SharpSpring is led by its two co-founders, Rick Carlson (current CEO) and Travis Whitton (current CTO). I think they have been around long enough to understand the business and its challenges.

Recently, Scott Miller joined SharpSpring’s board. Scott is an investor. He manages Greenhaven Road, which owns a large portion of SharpSpring and led the company’s funding round for the Perfect Audience acquisition. I view Scott’s involvement with SharpSpring’s board as positive because he’s smart and a clear-thinker. Here’s what he said in his last investor letter (talking about SharpSpring’s measures to deal with COVID-19):

“As a SharpSpring board member, I have a front-row seat to the process. Choices have been made to cut in some areas and invest in other areas. Will they be right? Will they be enough? Time will tell, but this is a smart and scrappy team, and my confidence in management has only increased.” Scott Miller

Valuation

SharpSpring’s valuation is tricky. The company is in growth mode and has yet to turn a profit. There’s incredible upside potential, but the business risk is high. If SharpSpring mirrors HubSpot (not in size, but in some financial metrics), there’s potential for a multi-bagger. However, management has to execute, and there are many moving parts to the story.

SharpSpring has a strong liquidity position, which is reassuring. In the balance sheet, ~$15mm in net cash, and close to no debt ($1.9mm, excluding lease liabilities). The business is asset-light. CapEx requirements are minimal ($1-2mm a year). Most of SharpSpring’s cash burn comes from operating expenses, which reflect strong investments in growth ($11.8mm S&M in 2019) and innovation ($5.0mm R&D in 2019).

To turn a profit, SharpSpring depends on attracting customers, increasing ARPU, decreasing CAC and churn rates, and realizing operating leverage. If it succeeds in all of these metrics, the company is worth multiples of its current value. If it succeeds in most of them, the investment case is there. If it fails most of them, we’ve fallen for a growth trap.

Here’s how I approached SharpSpring’s valuation.

I’ve used HubSpot’s and SharpSpring’s historic financials and guidance as a benchmark. I’ve adopted a cautious view relative to that benchmark, using assumptions that I believe SharpSpring is likely to achieve, such as:

CAC trending towards $8,500.

Gross margins trending towards 75%, R&D trending towards 20% of sales, and G&A trending towards 15% of sales.

1,100 agencies added annually (in line with SharpSpring’s 3-year average)

Some of my other assumptions were mentioned throughout this report.

I’ve also considered the impact of COVID-19 through lower agency acquisition in 2020 (300), a $6mm reduction in operating expenses, and an additional $5mm in cash obtained from accelerated tax refunds and from the Paycheck Protection Program (PPP).

My fair value estimate is the blend of a DCF valuation and a sum-of-the-parts valuation. The SOTP valuation has slightly tweaked and simplified assumptions for some metrics, such as flat gross margins and CAC, and linear OPEX growth. I use SharpSpring’s diluted net cash and diluted shares in my valuation.

My valuation implies a 3x P/Sales multiple over my estimate of $26.5mm 2020 revenue (SharpSpring’s 2020 revenue guidance is $30-31mm). This is a low sales multiple compared to deals done in the space.

To cite a few (multiples are approximate):

2013: Adobe acquired Neolane for 10x, SalesForce acquired ExactTarget for 8.5x, Oracle acquired Eloqua for 9.5x and Responsys for 7x.

2014: IBM acquired Silverpop for 3x.

2016: Vista Partners acquired Marketo for 6.5x, Web.com acquired Yodle for 1.75x

2018: Adobe acquired Marketo for 12x.

In addition, HubSpot, SharpSpring’s best comp, trades at a P/Sales multiple of 7.6x (5-year average of 7.7x).

I justify my lower sales multiple on:

1) SharpSpring’s niche market (focus on agencies vs. directly targeting SMBs), which yields a different long-term growth profile and adds uncertainty regarding its business strategy.

2) High business risk, because of low barriers to entry, a fragmented and competitive industry, and SharpSpring still being a micro-cap company (<$30mm annual sales).

3) The uncertain market environment due to the COVID-19 pandemic, which demotes past transactions as valid benchmarks.

Conclusion

SharpSpring is trading at $7.34/share, an 18% premium to my fair value estimate.

I don’t think the market value is absurd; SharpSpring could be worth multiples of that. The business is attractive in many ways: growing industry, clear potential for margin expansion, low capital requirements, and capable management team.

However, SharpSpring is not a quality company. It still has to prove its business model, threatened by competition. Business risk is high, and I prefer to lean on the safe side, waiting for a better entry point for an attractive risk-reward ratio.

Next Steps

Here’s what I’ll watch out for:

Evolution in key metrics: CAC, Churn Rates, ARPU, Gross Margins.

SharpSpring’s success in implementing price increases

Agency and Direct Customer additions

Integration with Perfect Audience (cross-selling opportunities, growth of the platform, etc.).