#7 The Curious Case of Inflation

#7 The Curious Case of Inflation

Plus: introducing FP's portfolio and portfolio management playbook

In this edition, I talk about dumping airlines and acronyms.

Hey Folks,

The recent market decline was good and bad. Good because I bought stocks at reasonable prices. Bad because I started this newsletter two months ago and didn’t have time to analyze more stocks in my watchlist (HERE). So, I wasted opportunities.

The net effect is that I started building FP’s portfolio earlier than I’d expected.

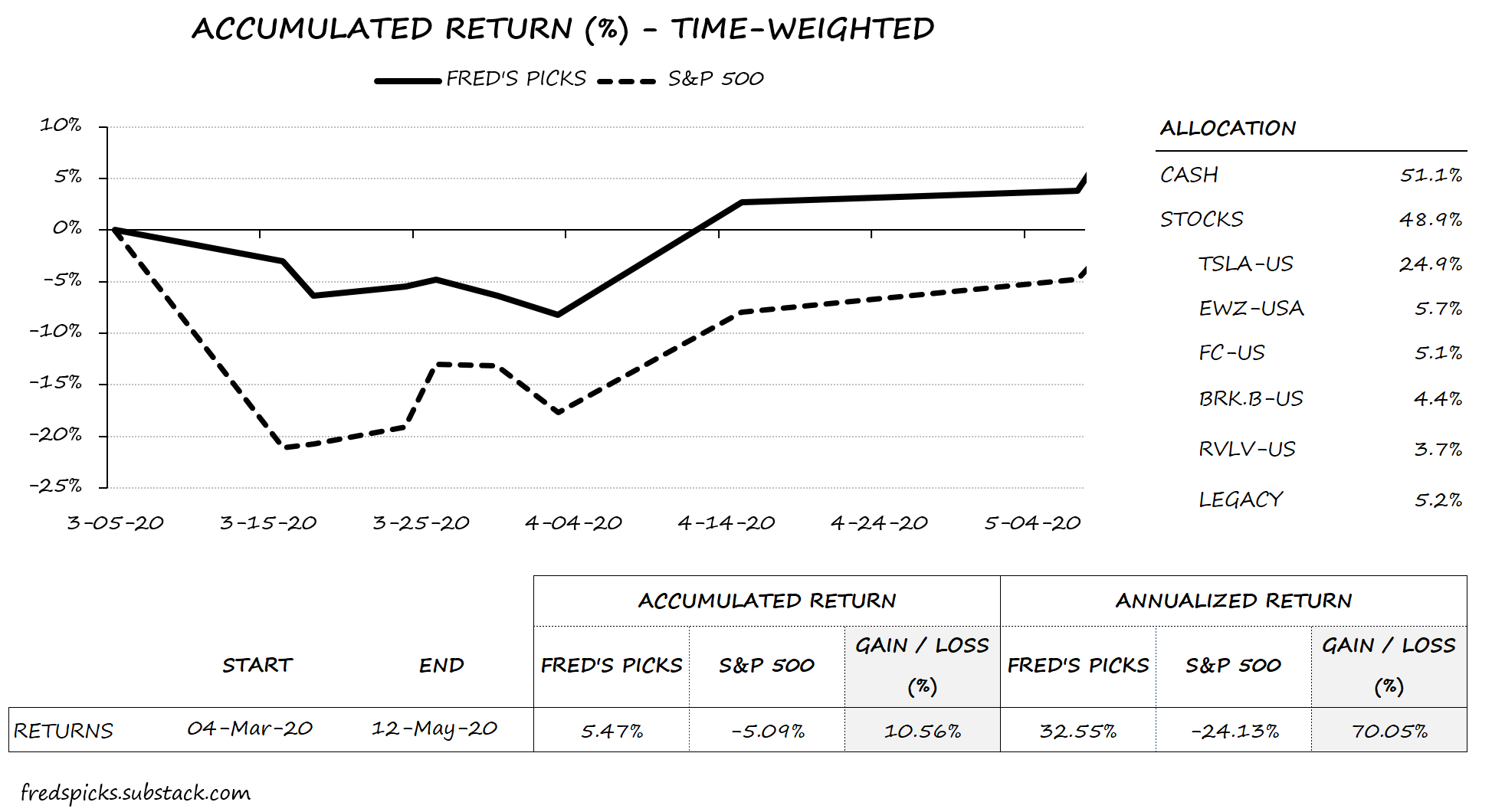

Here’s how it looks now:

Going forward, I’ll provide portfolio updates every quarter or if anything material changes.

Why Have a Model Portfolio?

Investing is hard. Stock picking is only a part of investing. Returns depend more on allocation, position-sizing, and execution. You can do good valuation work and pick a fantastic stock but still have terrible returns if you buy or sell the wrong quantity at the wrong time.

Keeping a stock watchlist is useful because I can follow companies I’ve analyzed, monitor prices, and gather feedback on my investment theses shortcomings. However, a watchlist ignores trading decisions in the context of a portfolio. Trading decisions are the hardest because they are subject to behavioral biases. As such, a watchlist fails to provide essential feedback on my investment process.

Without feedback, a process can’t improve. FP’s model portfolio will give me (and you, reader) a better chance to track performance and learn from it.

Portfolio Commentary

Cash: I’ll deploy some money as I enter new positions. A large cash balance now isn’t bad. It provides optionality in the face of uncertainty. Still, I’m wary of inflation. I’m aiming for a sub-20% cash balance.

Tesla: The stock appreciated 56%. I’ll gradually trim the position if it grows too much, and I have something else to buy.

Others: Legacy refers to minor positions I’d owned before starting the watchlist. They aren’t relevant for now as I’m reviewing them.

The Curious Case of Inflation

The COVID-19 pandemic lingers on. There’s no vaccine and no proven effective treatment. Some argue for a reopening, some reason for extending the lock-down. If we open now, will there be a second wave of infections? Will the world return to normal, or to a new normal?

No one knows, but markets are ok with that. Everything is closed, unemployment skyrocketed, and companies are leveraged to the bone. Still, Warren Buffett can’t find stocks to buy.

Dr. Michael Burry, commonly known as Christian Bale from The Big Short, sounds intriguing (perhaps because of all these acronyms I had to google):

Translation: the stock market is rising because investors have nowhere else to put their money since interest rates are zero (or negative). And investors have a herd mentality, so they fear missing out on the stock market rally. That may explain the near-all-time-high earnings yield spread of small-cap stocks vs. large-cap stocks (investors are hoarding in large-caps). Dr. Burry adds that if demand returns and supply can’t keep up, inflation awaits.

At least that’s my interpretation of his tweet.

Staying in the topic of inflation: Ray Dalio thinks “printing and devaluing money is the easiest way out of a debt crisis”. In case you didn’t notice, we’re in a debt crisis and we’re printing money. So, cash may not be that safe:

While people tend to think that a currency is pretty much a permanent thing and believe that “cash” is the safe asset to hold, that’s not true because all currencies devalue or die and when they do cash and bonds (which are promises to receive currency) are devalued or wiped out. That is because printing a lot of currency and devaluing debt is the most expedient way of reducing or wiping out debt burdens. - Ray Dalio

Inflation is tricky. According to Dalio, more money and credit reduce the value of money but relieve debt burdens. This situation can go two ways:

Money finds a way to increase productivity and profits, and real stock prices rise. In this case, it’s possible to grow out of the debt, and stop devaluing money, which is good.

Money is so devalued that capital flies to inflation-hedged assets and other currencies, and central banks either raise interest rates (economy suffers) or print more money (reinforces inflation in a vicious cycle), which is bad.

Yes, I know. It’s all kind of confusing. Economists don’t fully understand this, I don’t understand this, and there’s really no point in trying to predict inflation or a recession. But here’s what I think:

Holding some cash is always good, but keep an eye on inflation.

In this uncertain environment, strong balance sheets and business quality are paramount.

Holding quality stocks is a natural hedge against inflation. Good businesses are good for a reason: they should have the pricing power to adjust to an inflationary environment.

FP’s Portfolio Management Playbook

Only three things can happen to the price of a stock you own: decrease, increase, or stay the same.

1) Stock price decreases

FP playbook: Sell everything, or buy more.

Berkshire Hathaway had its annual shareholder meeting, and Warren Buffett revealed he dumped his airline stocks. At the end of 2019, Berkshire owned roughly 10% of Delta, American Airlines, Southwest, and United.

Before the meeting, people speculated Berkshire could have scooped a bunch of airline stocks in the cheap. That would make sense if Buffett still believed in the business. But COVID-19 changed his mind:

“I just decided that I’d made a mistake in evaluating. That was an understandable mistake. It was a probability-weighted decision when we bought that, we were getting an attractive amount for our money when investing across the airlines business. (…) And it turned out I was wrong about that business. (…) The airline business, and I may be wrong and I hope I’m wrong, but I think it changed in a very major way.” - Warren Buffett

Berkshire sold its positions entirely. As soon as Buffett smelled fire, he went for the fire exit.

When we sell something, very often it’s going to be our entire stake. I mean we don’t trim positions. When we change our mind, we don’t take half measures or anything of the sort. - Warren Buffett

Buffett knows this table:

Two conclusions:

Cut your losses soon.

Sometimes, price drops are good for averaging down.

As a general rule, you should dump everything as fast as you can. “Cut your losses short” is a known maxim, but most investors fail to execute it. The ability to take losses is a rare trait:

Soros is also the best loss taker I’ve ever seen. He doesn’t care whether he wins or loses on a trade. If a trade doesn’t work, he’s confident enough about his ability to win on other trades that he can easily walk away from the position. There are a lot of shoes on the shelf; wear only the ones that fit. If you’re extremely confident, taking a loss doesn’t bother you. – Stanley Druckenmiller

But, on some occasions, you should buy more. If you believe in the stock and confirm your thesis hasn’t changed, a 50% drop is a path for a 100% gain.

The simple rule is that there’s no “sell some” or “hold” option. If you don’t buy more, you’ve lost conviction. Holding the stock is just a way to fool yourself because you don’t want to realize a loss.

Scenario 2: Stock price increases

FP playbook: Gradual trimming.

The first rule of compounding is to never interrupt it unnecessarily – Charlie Munger

There’s a temptation to sell once a stock price increases. You know, “a bird in the hand is worth two in the bush” kind of thinking. There are two problems with that approach:

You give up having big winners in your portfolio.

You need to find a better place to park your money.

The problem is that to achieve a multi-bagger in the portfolio, you have to hold a multi-bagger. And if you want it to change your life, you need to hold a lot of it. Don’t bother finding the next multi-bagger if you aren’t going to develop the conviction to hold it. – Ian Cassell

Having a multi-bagger in your portfolio implies buying a stock at price X, and holding it through 3X, 5X, 10X. To get there, the stock needs to surprise you. It will reach your original fair value estimate and far surpass it. Fundamentals will change, and you’ll have to keep reassessing your investment thesis and assumptions.

Along the way, you’ll have plenty of reasons to sell based on valuation. You could’ve bought Amazon stock in 2012 for $200 and a rich EV/EBITDA of 35x. You could have sold it in 2014 for $400 and an even richer EV/EBITDA of 55x. Not bad: 100% gain, 41% annualized. You would’ve thought it was time to realize your gains and move on.

But you would’ve missed Amazon’s incredible run to $2,300/share in 2020. You exchanged a 1000% gain in six years for a 100% gain in two years.

100% in two years is nice. 1000% in six years builds wealth. Investing is about building wealth.

It’s unwise to sell based on valuation because you give up having big winners on your portfolio (I do think it’s wise to sell based on quality). You can expect few names in a portfolio to account for a disproportionate share of its returns. It’s Pareto’s Law. No portfolio is successful if it doesn’t leave a chance for big winners.

Sure, we have the benefit of hindsight, and Amazon could have stalled at $400/share for years to come. But you don’t need every stock to be a winner, only a few.

Besides, once you sell, you need to allocate capital somewhere else. You need idea flow, which is high maintenance. You’ll have one more buying decision to make, and you need to buy something better than what you just sold.

You’re steered to action and prone to error. Not an ideal setup.

I think a good approach is to trim the position gradually. Benefits are two-fold: you keep the stock in your portfolio, holding unto its upside potential, and you steadily allocate capital to other ideas, decreasing valuation risk and exposure.

Scenario 3: Stock price stays the same

FP playbook: Do nothing.

“Most of the money I make is in the third or fourth year that I’ve owned something.” – Peter Lynch

If a stock price doesn’t move and the thesis hasn’t changed, it’s better to do nothing.

Doing nothing requires discipline. When a stock price stays the same, we second-guess ourselves. Doing something is a way to justify ourselves we’re doing our work the best we can.

Today we have excessive access to information. The more information, the lower the signal-to-noise ratio, and the more you’re compelled to act.

It’s hard to resist action. That’s why time-horizon advantage is a thing. Though almost all investors say they think long-term, reality shows they don’t. The market is obsessed with quarterly earnings and short-term price movements.

In investing, doing nothing is an advantage because:

You take the time to know what you own, which prepares you to act when needed (e.g., if something fundamental in your investment thesis changes).

You spend more time researching new ideas and don’t lose sight of the big picture.

Things don’t happen linearly. A stock price can stay the same for years, then rise. Fundamentals backfill, negative investor sentiment subsides, management improves communication with the market, institutional investors buy-in, a new economic cycle begins, or some unknown catalyst occurs.

When you take action, you’re setting yourself for mistakes. What you’re about to do should leave you better than before. Often, that’s an elusive watermark.

What I’m Reading

Don’t be the best, be the only: “To make something good, just do it. To make something great, just re-do it, re-do it, re-do it. The secret to making fine things is in remaking them.”

I wish I was a goat farmer: “Mark Spitznagel’s $4.3 billion Universa Investments has waited 12 years for a perfect catastrophe. (…) After the March payday, its flagship Black Swan fund has produced a mean annual return on invested capital of 76%* since the firm was created in 2008.”

If you don’t build stuff there’s no stuff: “In fact, I think building is how we reboot the American dream. The things we build in huge quantities, like computers and TVs, drop rapidly in price. The things we don’t, like housing, schools, and hospitals, skyrocket in price. What’s the American dream? The opportunity to have a home of your own, and a family you can provide for. We need to break the rapidly escalating price curves for housing, education, and healthcare, to make sure that every American can realize the dream, and the only way to do that is to build.”

If you liked this edition,

Subscribe and share!

Stay well,

Fred.

Watchlist

You can find my updated watchlist HERE.

Hi Fred, great note - as always.

On top of the reasons you pointed out not to sell a stock that has appreciated before thorough analysis, I would add another one: transaction costs. For instance, unless you are investing through a tax free account, you would be anticipating tax payments and reducing your asset base.

I noticed RVLV in your watchlist is above your target price. How would the rationale above apply to this stock specifically? Did the fundamentals change?

Thanks,