What's Going On With MSOS?

What's Going On With MSOS?

Plus: a quick portfolio update.

Hey folks,

Two months ago, I talked about the MSOS ETF and why I had bought it. Well, that wasn’t my best decision. I have (so far) lost almost 20% of my average cost.

My options now are to (1) exit the position, (2) hold, or (3) buy more.

I already acted on #3 as I bought more on the way down. I stopped because it felt like I was trying to catch a falling knife, and MSOS is already a good chunk of my portfolio.

That leaves me with #1 or #2. To decide between them, I have to check if my investment thesis went sour and what’s the reason MSOS declined.

Has my investment thesis changed?

My core thesis was:

US MSOs are trading at a significant valuation gap to Canadian LPs;

This valuation gap is explained by constraints on accessing capital;

These constraints will go away when MSOS uplist to major US stock exchanges;

The valuation gap will close, and MSOS will become overvalued;

The cherry on top is that MSOs are growing triple digits with high margins, so there’s also a fundamental case to be made here.

Nothing changed on that first point. US MSOs continue to trade at a valuation gap to Canadian LPs.

I still think a higher cost of capital explains this valuation gap. Consider that US MSOs have higher growth rates and better profitability than Canadian LPs. MSOs also have access to a much larger market.

This valuation gap will close once regulations change. The critical catalyst here is US MSOs up-listing to major US stock exchanges. It’s a matter of when not if.

One could argue that regulatory changes are coming later than expected. That’s a valid concern.

Regulatory delays, however, don’t kill my thesis. It’s true that current regulations hinder capital flows to the sector and limit the total size of the US market. But simultaneously, they insulate large US MSOs from competition.

While regulations don’t change, MSOs will increase penetration in states that have already legalized cannabis and expand into new states that are doing so. This is a tailwind for their fundamentals, as MSOs can compound value and increase their moats. 50% EBITDA margins aren’t sustainable in the long run, but I’ll take them for now.

In my previous write-up, I said:

While I’m not sure if they (MSOs) are undervalued, they certainly aren’t overvalued. Consider that MSOs are growing triple digits despite their state-fragmented operations.

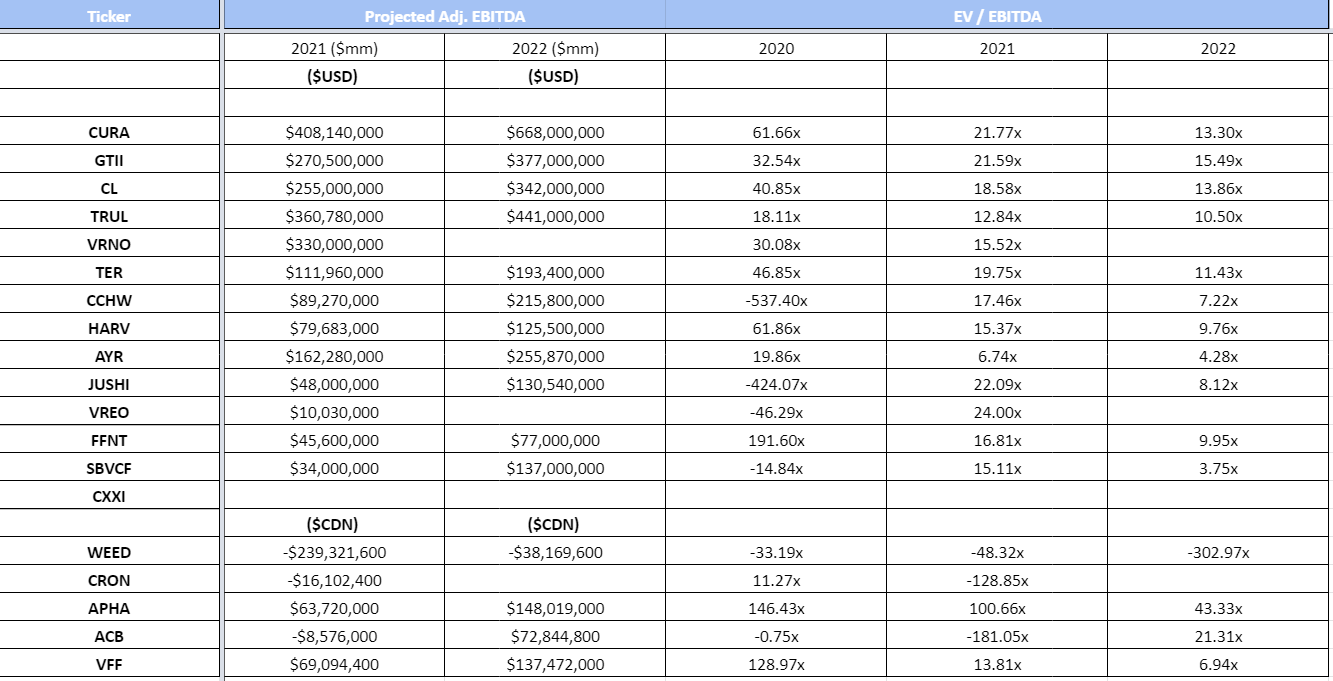

Considering the recent pullback in prices and recent quarterly results—which were all good—I now think that US MSOs are undervalued. These businesses are growing at SaaS-like rates, but the stocks are trading at 15-20x EV/EBITDA. Though I wouldn’t take this number at face value (adjustments should be made when interpreting multiples in this industry)1, there’s a margin of safety indicating there’s good value in this pot.

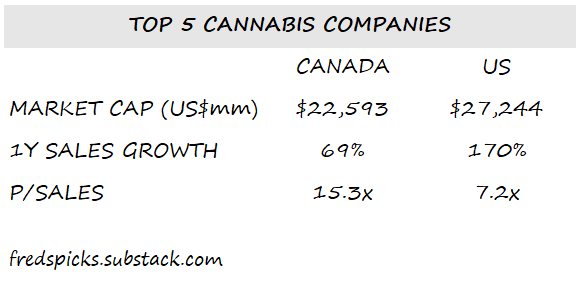

This picture from CannaConfidential is great:

What Happened Then?

There’s always something happening in the markets. Good buying opportunities are often created through events that are unconnected to the fundamental outlook of entire sectors or individual stocks.

Over the last few months, the constituents of MSOS were caught up amid bad market sentiment towards growth stocks, with concerns over inflation and rising interest rates. Also, expectations for a change in regulations might have built up too far in anticipation of a changing political environment. MSOS reached all-time highs, so it was time for some to realize gains, impacting sentiment and short-term price action.

I paid too much when I made my first buy decision. It’s easy to conclude that in hindsight, but I probably could have waited for a better entry point or built my position more slowly.

This is now the past, and the past is sunk, be it costs or gains—only the future matters.

Looking Ahead

The investment case for MSOS remains compelling, especially on a longer time horizon. US cannabis companies continue to grow at high rates. Valuations are reasonable. As growth materializes, these stocks will compound value. To get a good return, multiple expansion isn’t needed. There are also several catalysts laying ahead, such as more states legalizing cannabis, an up-listing to major US exchanges, or full-blown federal legalization.

Patience is key. I’m holding.

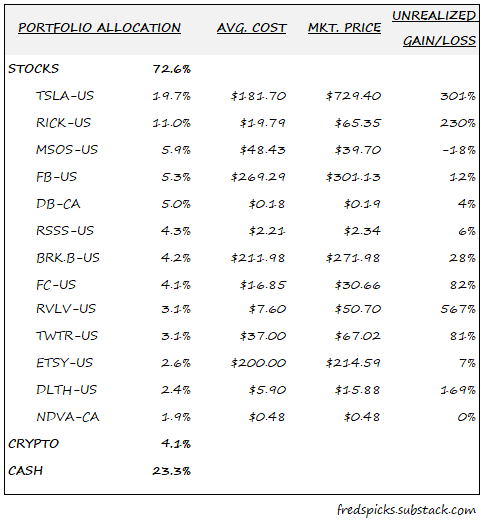

Portfolio Update

Year to date return: +21%

New positions

Decibel: A micro-cap cannabis company in Canada that’s flying under the radar. The business has a valuable brand and cultivation, manufacturing, and retail facilities. The cost structure is lean, and the company just reached break-even. Sales are growing fast and Decibel is coming off a low revenue base. There’s no coverage, no consensus estimates, and barely any discussion around this name on Reddit, Twitter, or Seeking Alpha, which makes it difficult for market participants to realize that the stock is trading at a 60%-90% discount to peers. I think there’s a potential upside of +100%.

Indiva and Etsy: I’ll write more about those two names in the future. The first has a similar thesis as Decibel. The latter is a high-quality compounder.

Other Write-ups

The EV may be a off considering dilutive securities outstanding, and the EBITDA number is usually adjusted for share-based comp, which is an actual expense for shareholders.